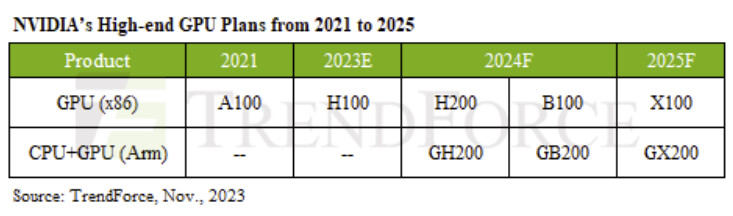

Blackwell Shipments Imminent, Total CoWoS Capacity Expected to Surge by Over 70% in 2025

TrendForce reports that NVIDIA's Hopper H100 began to see a reduction in shortages in 1Q24. The new H200 from the same platform is expected to gradually ramp in Q2, with the Blackwell platform entering the market in Q3 and expanding to data center customers in Q4. However, this year will still primarily focus on the Hopper platform, which includes the H100 and H200 product lines. The Blackwell platform—based on how far supply chain integration has progressed—is expected to start ramping up in Q4, accounting for less than 10% of the total high-end GPU market.

The die size of Blackwell platform chips like the B100 is twice that of the H100. As Blackwell becomes mainstream in 2025, the total capacity of TSMC's CoWoS is projected to grow by 150% in 2024 and by over 70% in 2025, with NVIDIA's demand occupying nearly half of this capacity. For HBM, the NVIDIA GPU platform's evolution sees the H100 primarily using 80 GB of HBM3, while the 2025 B200 will feature 288 GB of HBM3e—a 3-4 fold increase in capacity per chip. The three major manufacturers' expansion plans indicate that HBM production volume will likely double by 2025.

The die size of Blackwell platform chips like the B100 is twice that of the H100. As Blackwell becomes mainstream in 2025, the total capacity of TSMC's CoWoS is projected to grow by 150% in 2024 and by over 70% in 2025, with NVIDIA's demand occupying nearly half of this capacity. For HBM, the NVIDIA GPU platform's evolution sees the H100 primarily using 80 GB of HBM3, while the 2025 B200 will feature 288 GB of HBM3e—a 3-4 fold increase in capacity per chip. The three major manufacturers' expansion plans indicate that HBM production volume will likely double by 2025.